Featured

Roth IRA Contribution and Income Limits for 2025

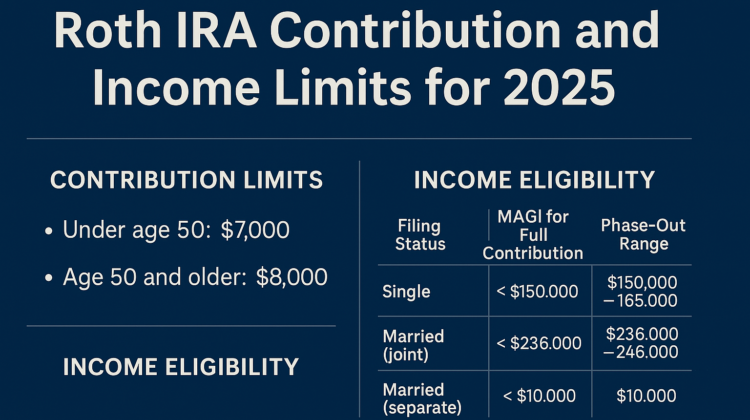

Roth IRAs 2025 Key Points For 2025, Roth IRA contribution limits are $7,000 for those under 50 and $8,000 for those 50 and older (includes a $1,000 catch-up contribution). Eligibility depends on income: singles can contribute fully with MAGI under $150,000, and married couples filing jointly under $236,000. Income phase-outs apply for partial contributions, with…

Continue Reading Roth IRA Contribution and Income Limits for 2025

Spotlight

Real Estate Syndication in Indianapolis: Unlocking Investment Potential

Real Estate Syndication in Indianapolis When it comes to building wealth through property investment, few strategies are as dynamic and accessible as real estate syndication. In Indianapolis, this…

Continue Reading Real Estate Syndication in Indianapolis: Unlocking Investment Potential

Maximizing Your 401k at 55 | Retirement Strategies for Growth

Maximizing Your 401k at 55 | Retirement Strategies for Growth

Continue Reading Maximizing Your 401k at 55 | Retirement Strategies for Growth

Explore

Retirement Savings Options: Navigating the Path to a Secure Future

Planning for retirement is one of the most critical financial decisions individuals face. With the increasing life expectancy and rising cost of…

Continue Reading Retirement Savings Options: Navigating the Path to a Secure Future

Retirement Planning

Retirement planning

IRA and 401(k): Compare Your Retirement Options

When planning for retirement, understanding the different investment options available is crucial. Two popular choices are the Individual Retirement Account (IRA) and…

Continue Reading IRA and 401(k): Compare Your Retirement Options